- DAY TRADING 📈

- Posts

- Trump's 8 PM Ultimatum 🛢️

Trump's 8 PM Ultimatum 🛢️

One deadline, one strait, $112 oil, and a market that somehow keeps grinding higher

DayTrading Dispatch

April 07, 2026

Welcome back to the Day Trading newsletter 📈

Stocks just put together their fourth straight up session even as the U.S.-Iran war hits day 38, oil sits north of $112, and a presidential deadline expires tonight.

Either traders know something the rest of us don't, or this is the calmest panic we've ever seen.

Buckle up 👇️

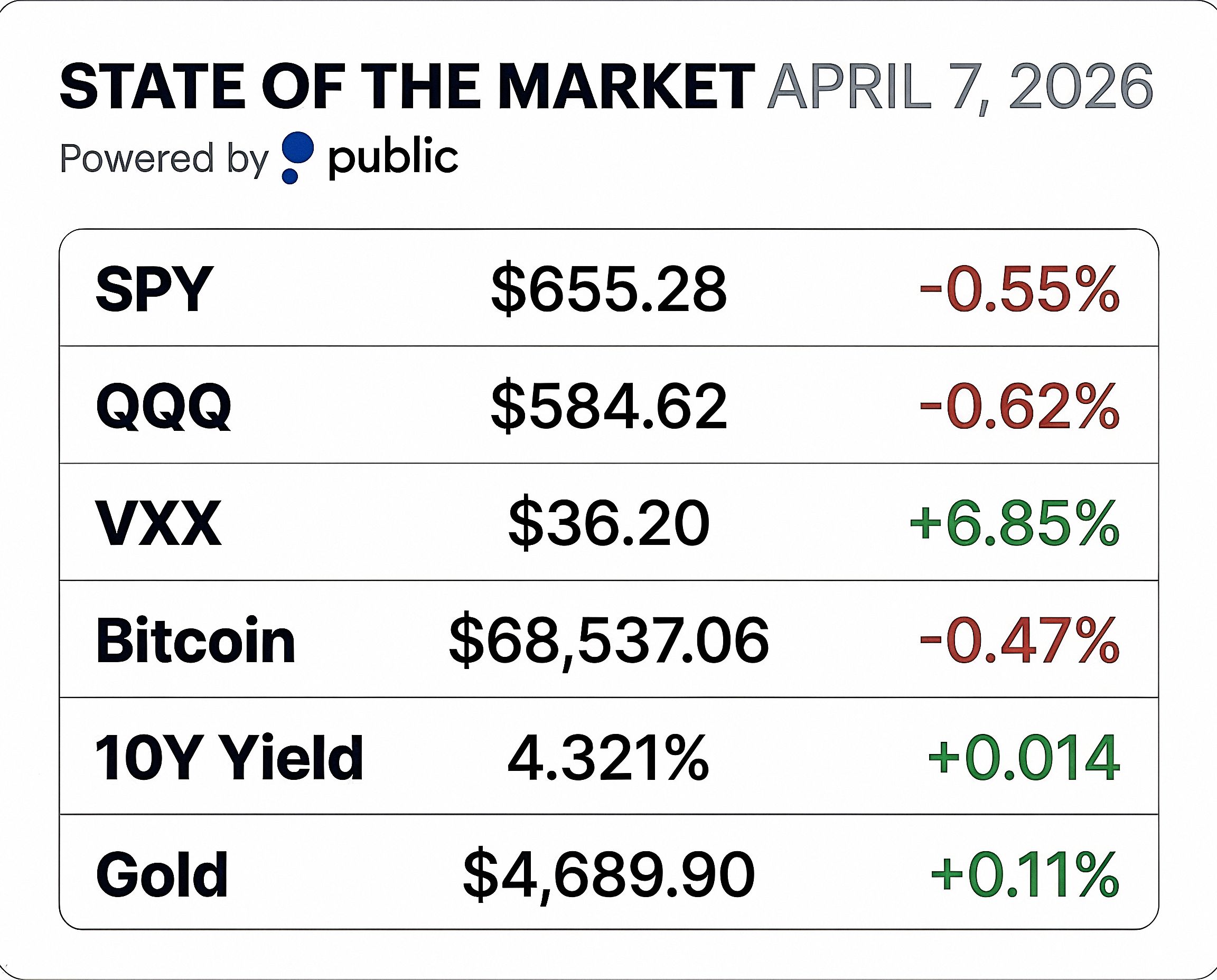

Data updated at 3:20 PM EST. For real-time market data, visit Public.

📉 March ISM Services came in at 54, down from 56.1 in February. The shock was inside the report: the Prices Paid Index jumped to 70.7, the highest reading since October 2022, while the Employment Index contracted to 45.2 from 51.8. ISM said respondents repeatedly cited fuel surcharges and Hormuz-linked supply disruptions as the drivers behind the price spike. (PR Newswire)

✈️ Jet fuel hit $4.88 a gallon, nearly double its level six months ago, and the NYSE Arca Airlines Index fell 12% last week. Analysts now estimate the fuel shock will add roughly $25 billion in unbudgeted costs across U.S. carriers in 2026. Delta is the relative winner thanks to its Monroe Energy refinery in Pennsylvania, which provides a natural hedge against the spike. (CNN)

⚙️ Trump's revamped steel, aluminum, and copper tariffs went live Monday, with a 50% duty on articles made entirely of those metals and 25% on derivative products. Certain electrical-grid and industrial equipment got a reduced 15% rate through 2027 to support domestic buildout. Steel and aluminum producers rallied on the news, while industrial users warned of immediate cost pass-through. (SupplyChainDive)

🔋 The Department of Energy issued an RFP April 1 for an additional 10-million-barrel emergency exchange from the Strategic Petroleum Reserve, on top of the 172 million barrels the U.S. is already releasing as its share of the IEA's record 400-million-barrel coordinated drawdown. IEA Executive Director Fatih Birol has repeatedly warned that April supply constraints will be "much worse" than March. (DOE)

🔼 Gold traded around $4,660 an ounce Monday, hovering near its all-time high as central bank buying and ETF inflows continue to pile in. J.P. Morgan now sees gold averaging roughly $5,055 in Q4, while Goldman Sachs lifted its end-2026 target to $5,400. Net inflows into gold-backed ETFs hit 78 tonnes in just the first two months of 2026. (FXLeaders)

🔴 Iran's 10-point response, routed through Pakistan, paired a 45-day ceasefire with a path toward reopening the Strait, sanctions relief, and reconstruction. Trump called the offer "significant" but "not good enough" and reiterated his Tuesday-night ultimatum. Egyptian and Pakistani diplomats are still shuttling between the two sides as the deadline approaches. (Aljazeera)

📉 JPMorgan analyst Ryan Brinkman reiterated his Underweight rating and $145 price target on Tesla Monday — implying roughly 60% downside from current levels — after Q1 deliveries of 358,023 came in below the ~365,000 consensus and inventory built by 50,363 units. Brinkman also flagged that Tesla's energy storage deployment fell 15% year-over-year to 8.8 GWh, well below the 14 GWh Wall Street expected. (CNBC)

President Trump set an 8 p.m. ET Tuesday deadline for Iran to reopen the Strait of Hormuz, warning Tehran would otherwise be "taken out in one night" with strikes on bridges, power plants, and other critical infrastructure.

Iran's counter — delivered to the U.S. through Pakistani intermediaries — was a 10-point proposal that included a 45-day ceasefire, a protocol for safe passage through the Strait, reconstruction funds, and the lifting of sanctions. Trump called it "significant" but "not good enough" and refused to back the 45-day pause.

What's strange is how the market is taking it.

The S&P 500 climbed 0.44% Monday to 6,611.83, its fourth straight session in the green, and S&P futures were flat overnight even as the deadline ticked closer. WTI crude settled at $112.41 — high, but well below the $130-plus levels traders feared two weeks ago.

Gold is hovering around $4,660 an ounce, near a record but not surging. The 10-year Treasury yield ticked down to 4.339%. Translation: bond and equity markets are pricing in a last-minute deal, not Armageddon.

The setup matters because the asymmetry is brutal. If Iran blinks before 8 p.m., oil could drop $10–15 a barrel overnight and risk assets rip. If it doesn't — and U.S. strikes hit Iranian infrastructure — every gap in the futures market opens against you.

This is the rare moment where the size of the move is roughly known, but the direction is a coin flip on a single headline.

What to watch: the 8 p.m. ET deadline itself, then the overnight crude tape in Asia, then Wednesday's FOMC minutes, which will tell us whether March's Fed was already starting to flinch on inflation before any of this began.

RATE TODAY’S EDITION

What did you think of today's newsletter?Let us know what you liked, what you didn't, and what you'd like to see in future editions. |

⚠️ Disclaimer: Not financial advice. Do your research before making any trades.