- DAY TRADING 📈

- Posts

- Powell pours cold water 🥶

Powell pours cold water 🥶

PLUS: PPI runs hot, and Micron crushes it after hours...

DayTrading Dispatch

March 19, 2026

Welcome back to the Day Trading newsletter 📈

The Fed held rates yesterday (no surprise) but the tone was anything but neutral.

Powell warned inflation isn't coming down as "hoped," the dot plot held at just one cut for 2026, and the Dow tanked 750 points to a new 2026 closing low.

Buckle up 👇️

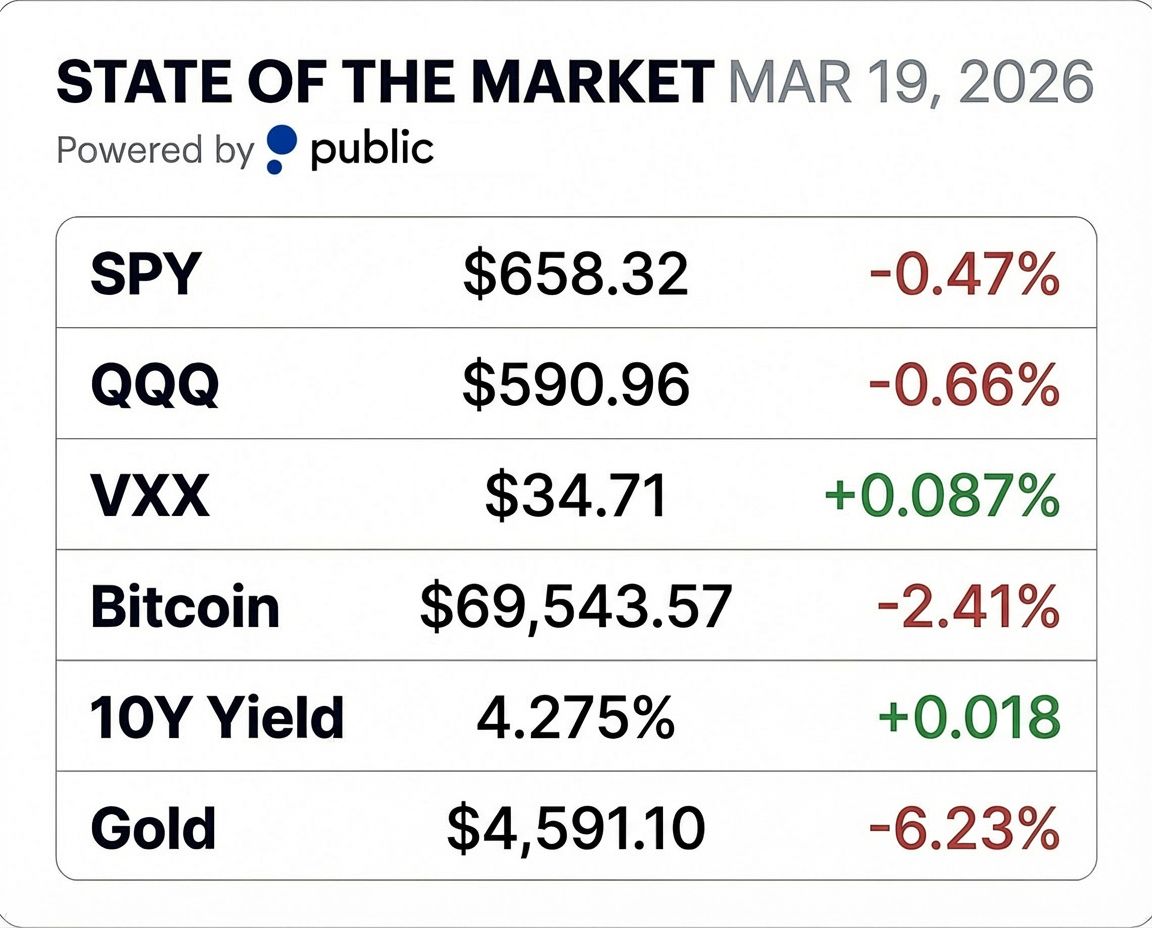

Data updated at 12:40 PM EST.

For real-time market data, visit Public.

📈 Micron demolished earnings after the bell: $23.86 billion in revenue (vs $20.07B expected), crushing estimates by nearly $4 billion. Q3 guidance was even more jaw-dropping. $33.5B in revenue with 81% gross margins and $19.15 EPS. The entire 2026 HBM supply is pre-sold. This is the clearest proof yet that AI hardware demand is real. (CNBC)

🤑 Nvidia projected $1 trillion in orders for Blackwell and Vera Rubin chips through 2027 at GTC this week (double last year's forecast). Huang unveiled the Groq 3 LPU from the $20B Groq acquisition, Vera Rubin shipping later this year with 10x performance per watt, and declared the "ChatGPT moment for autonomous driving" with new Uber, Hyundai, and BYD partnerships. Stock rose about 2%. (CNBC)

🔥 February PPI came in scorching hot. Producer prices jumped 0.7% month-over-month, with headline PPI at 3.4% year-over-year, the highest since February 2023. Core PPI hit 3.9%. The data landed Wednesday morning before the Fed decision, adding to the hawkish backdrop. Oil and tariffs are expected to push it even higher. (CNBC)

🚢 Trump waived the Jones Act for 60 days, a 1920 law requiring U.S.-built, U.S.-crewed ships for domestic transport. The move lets foreign tankers move oil between American ports to ease gas prices driven by the Iran war. It's the first time the act has been waived for oil outside of hurricane emergencies. (CNBC)

📉 The Dow dropped 750+ points Wednesday to a new 2026 closing low after Powell's press conference. The S&P fell 1.1% and is now nearly 6% below its January all-time high. The selloff accelerated into the close as oil surged back above $101 and bond yields rose. (Reuters)

📦️ FedEx reports earnings after the bell today and it's being watched as an economic barometer. The delivery giant's stock raced higher early in 2026 on rosy economic views, but the Iran war and surging oil have changed the calculus. Analysts expect EPS of $4.11-$4.15. Guidance will be the real tell on whether global trade is holding up. (Bloomberg)

The Fed held rates at 3.50-3.75% Wednesday (no surprise) but the real story was everything around it.

The updated dot plot maintained a median forecast of just one quarter-point cut for 2026, the same as December.

Powell then took the podium and delivered the most hawkish press conference of the year, warning that inflation is not coming down as much as "hoped" and saying explicitly: if the data doesn't improve, don't expect a cut.

The backdrop made it worse. February PPI landed that morning at 3.4% year-over-year (the hottest read since early 2023) with core at 3.9%.

Oil is still above $100 thanks to the Iran war. And the Fed's own updated projections showed officials raising their inflation forecast while lowering their growth outlook.

That's the textbook definition of stagflation risk, and Powell essentially acknowledged it without using the word.

Markets didn't take it well. The Dow dropped 750 points to a new 2026 closing low.

Futures pricing now shows the first cut isn't expected until at least September, more likely October, and even then just one.

With Kevin Warsh set to replace Powell as chair in May, this may have been one of Powell's final opportunities to set the tone.

He chose caution.

RATE TODAY’S EDITION

What did you think of today's newsletter?Let us know what you liked, what you didn't, and what you'd like to see in future editions. |

⚠️ Disclaimer: Not financial advice. Do your research before making any trades.